Some cool apartment constructing photos:

0802 | Howland Apartment Building | 2009 | East Side

Image by Facility Records | MSU Physical Plant

0802 | Howland Apartment Building | 2009 | East Side

If you would like to see far more houses click right here…

American Mailbox (Wakulla County, information pills Florida) .. Stroll Away From Debt For a Better Future

Image by marsmet461

One particular time, stomach my wife said to me, cost [imitating his wife] "Honey, the dryer is broken." [as himself] Did you examine the lint trap? [imitating his wife with a clueless face] Sit down, honey, I’ll check it. [as his wife] "Was there anything at all in there?" [as himself] Just a quilt. …Ron White …a/k/a Tater Salad..

.

……………………………………………………………………………………………………………………………………………………………………..

.

…..item 1A)…..The Huffingtonpost…..HUFFPOST Enterprise….Shifting the Focus From "Strategic Default" to "Prudent Walkaway"

Nicholas CarrollAuthor, "Walk Away From Debt for a Far better Future"

Posted: March 24, 2011 07:38 PM

www.huffingtonpost.com/nicholas-carroll/shifting-the-focu…

A "strategic default" currently signifies walking away from an underwater home even though the owner could afford to pay the mortgage. Nonetheless, this represents far much less than half of walkaways. The vast majority of foreclosures come about to folks who can not afford to spend the mortgage.

Portrayals of strategic default in 2009 were usually of property owners who "used their house as an ATM," or "deadbeats." Even news stories describing the good side of default didn’t entirely shake these images. 1 of the earliest semi-positive stories was in the Wall St. Journal, titled "American Dream two: Default, Then Rent." This short article described a couple who had defaulted, cut their housing costs from almost ,000/month to just more than ,000/month, and were living in a larger house with "a swimming pool with 3 waterfalls." Yet another strategic defaulter in the identical post identified the rewards of default-and-rent included the discretionary income to go out to dinner a lot more often, and hang on to his series-6 BMW.

These are not the people I meet in the course of interviewing and writing about surviving difficult times. The folks I meet are laid off, or from two incomes down to 1, or on their way to medical bankruptcy. They can’t envision a swimming pool, a lot much less a waterfall — they just have bills they can’t pay, one particular of which is the mortgage. Some are slow in adjusting to the "new typical," and nevertheless consume out routinely, but other individuals have currently cut back to consuming out four occasions a year.

Their residence could be underwater — or they could have equity. Usually it does not matter, when the bottom line is that they have to decide on between the mortgage and medical insurance coverage — because losing health-related insurance in America is potentially lethal.

For this group, it is not a matter of cunningly defaulting to keep a latte-sipping life-style. It is a matter of prudently walking away from the mortgage that is dragging their family and future under the waves.

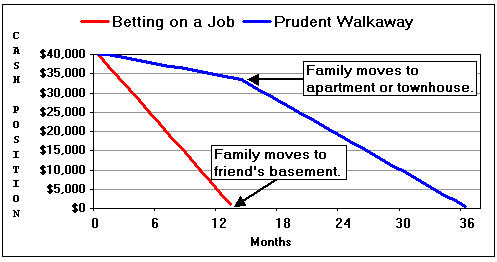

The benefit for people who act both prudently and decisively can be startling. Taking a relatively standard instance from men and women I’ve interviewed, this is the family’s monetary circumstance:

Key earnings of ,000 net per month is gone, with a single laid off.

Secondary earnings of ,000 net is nonetheless coming in.

,000 in cash and savings, such as the 401K.

,000 in credit card debt.

One particular automobile fully paid for.

Second car — ,000 owed.

They have completed a careful financial projection. The total monthly expenditures are ,000, correct down to the last dime — which consists of ,500/month on mortgage and credit card bills. That says that if the principal breadwinner is not fully employed in 14 months, they will lose the property — and of course take a dip in their credit rating. And if the job does not come till the 13th month, it had greater be at the identical salary as the earlier job, or they’ll shed the house anyway.

Situation A: Betting on a job, and continuing to pay the mortgage (a.k.a. "doing the correct issue," according to the moralists). They guess that they will be fully employed again in time to save the home. They continue paying mortgage, vehicle payments, and minimum monthly credit card payments. If their bet is incorrect, their trajectory is shown by the red line below.

Situation B: Prudently walking away. They make a decision that obtaining a job may require a career shift or relocation, with some time and income invested in re-education. They instantly quit paying the mortgage and credit card payments. In this scenario, they cut their expenditures by ,500/month (which rises to ,500/month when they move out and start off paying rent). If there is genuine equity in their financed vehicle, they sell it and buy a employed auto to replace it.

.

………………………………………………………..

Betting on a Job – Prudent Walkaway….

images.huffingtonpost.com/2011-03-22-prudenthomewalkaway.jpg

………………………………………………………..

.

………………………………………………………..

{kind=link}

Worksheet on the internet in MS Excel format or PDF

www.walkawayfromdebt.com/worksheets&charts.html

.

……………………………………………………..

The difference among A and B is amazing. If the family bets the key bread-winner will be working within the year and is incorrect, they could be leaving their property with out enough income to rent a decent apartment in 14 months — exhausted, frightened, and possibly operating on bald tires. (Men and women who "do the right factor" tend to leave long prior to they truly get legal notice to move.)

The family members that bets the key bread-winner will not discover a job in 13 months and stops paying the debts will be leaving their residence with ,000 money in hand, move to a rental (generally in the very same school district, if need be), and will have three years for the primary bread-winner to discover a job. And that’s their worst situation — it really is very most likely they will be in the house for 18-24 months without having making any mortgage payments.

Conclusion: when the writing is on the wall, the very best program is typically a prudent walkaway — an escape to the future, equipped with enough cash to get there.

.

………………………………………………………………………………………………………………………………………………………………………

.

…..item 1B)…..The Strategic Default Monitor….

Sunday, March six, 2011

The 3 Need to Send Debt Defense Letters

The 3 Must Send Letters

The following are the 3 "Must Send" Debt Defense letters. This means that at all instances you need to send any of these letters to any debt collection organization or the original lender that contacts you

Read more »

Posted by Grinnin Skinny at three:03 AM two comments

.

………………………………………………………

.

Monday, January 24, 2011

Think about Employing A Mortgage Calculator, Amortization Table And House Value Data For A Strategic Default

Portion of our job at strategicdefault.org is to critique other viewpoints about strategic default. This current post is inspired by yet another post we located while researching the universe of articles on strategic defaults and foreclosures.

We discovered this post entitled : “Should I Do a Strategic Default on my Mortgage?” by JLP in his blog All Financial Matters posted December two, 2010.

This question was posed by a reader of JLP’s weblog. The question and answer are as follows:

"I purchased my condo at precisely the incorrect time. I didn’t, nonetheless, listen to everyone telling me I could afford to buy much more. I did a straight 30 year fixed that I could afford in reality. Of course I am extremely underwater on my mortgage now. It is depressing, needless to say, and even more so when I really feel as if my taxes are helping folks who didn’t “do items the correct way” and some firms who seemed to have contributed tremendously to the difficulty and are not being held accountable…I reside in Illinois, western burbs of Chicago…I purchased for 9,000, now owe two,000 and the most current sale was ,000…30 year, six.75% (which was excellent then!) percent…When I bought I planned on staying five years or so and moving up (didn’t absolutely everyone?). I don’t *want* to move. I confident wish I could buy some of the homes on the market now though! For what I paid? I bring home (right after taxes) about ,000 a year. My mortgage + PMI + escrow is nearly ,100…I know there are people in much worse shape. If I lost my job this whine about underwater wouldn’t even exist, you know? Nonetheless – just the although of paying even More out when I really feel like I am not getting any advantage is upsetting, depressing."

The writer, JLP answers as follows:

Read a lot more »

Posted by Grinnin Skinny at 12:06 AM five comments

Labels: a diji, amortization, augustine a diji, augustine ademola diji, augustine diji, ken mcallion, ken mccallion, kenneth mccallion, mortgage calculator, property value, strategic default

.

……………………………………………………………………………………………………………………………………………………………………….

.

…..item 1C)…..The Strategic Default Monitor…The three Have to Send Debt Defense Letters

Sunday, March six, 2011

www.strategicdefault.org/2011/03/three-should-send-debt-defense…

.

………………………………………………………………………………………………………………………………………………………………………

.

.

.

Far more excellent homes click right here…